What next for Ljubljana office?

What next for Ljubljana office? Translation of an article that appeared in Finance, Slovenia’s daily financial newspaper, on Tuesday 29th may 2018

By Jacqueline Stuart

Very little quality office space available

The office market in Ljubljana is under developed, with only a small number of quality buildings. The current office stock in Ljubljana comprises around one million square metres, and consists of mainly Class B office space, which does not meet international standards. Most buildings were constructed during the days when Slovenia belonged to Yugoslavia and are now outdated, with insufficient parking, small inefficient floorplates, and poor energy efficiency. Many were sold in parts to individual owners as condominiums, and it is now difficult to get all owners to agree to necessary works. Tivoli Center and Eurocenter are the only two office buildings in the city centre that meet Class A standards. Most Class A buildings elsewhere in the city are full, or nearly full.

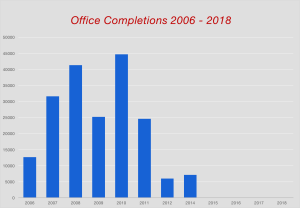

The evolution of the office market

When Slovenia joined the EU in 2004, two important changes had a big impact on the Ljubljana office market. First many international companies opened branch offices, creating demand for quality office space. There were very few Class A office buildings back then, and space traded at up to 22€/m2/month. Second, local banks got greater access to interbank borrowing which made it easier for local developers to raise finance for new projects. Office buildings sprung up all over Ljubljana in response to these changes, some in quite unlikely places. In 2008, over 41,000m2 came to market – a large amount for a small city.

Predictably, the oversupply of new buildings caused a crisis in the office market and rents plunged. Office developers were forced to give generous incentives to tenants including rent free periods, discounts, and free fit outs. It has taken many years to fill up the new buildings, but now there is little space left.

The difference between Class A and Class B

Most occupiers would choose a Class B building in a good location over a Class A building in a poor location. Proximity to restaurants, shops, post office, business hotels and other amenities is considered important. The main difference between Classes A and B is the age of the building. Anything over 15 years old in Ljubljana is automatically considered Class B. The main disadvantage of Class B buildings are that they don’t have raised floors or suspended ceilings, relying on trunking round the perimeter of the office suite for distribution of cables. HVAC systems can be inefficient resulting in poor quality air. There is often insufficient parking. Many Class B buildings could be renovated and improved, but in Ljubljana this is rarely possible given the fragmented ownership of the properties. Most companies consider their office premises an important part of their corporate image, and they like to be in smart new buildings. In Ljubljana however, tenants usually have to compromise.

Where is the central business district?

Most capital cities have a central business district, which is usually near the city centre. A CBD in Ljubljana has never developed however. This is for two reasons. First there is little land available round the city centre for new developments. Second, many companies are deterred from Ljubljana’s city centre because of the lack of parking, and the expense of what little is available. Traffic congestion is also an issue. In Ljubljana, a large percentage of office workers drive to work, compared to London where only 35% take their car. The nearest thing Ljubljana has to a central business district is north Bežigrad, with 7 notable office buildings clustered around the Austria Trend Hotel.

City centre occupiers

Approximately 50% of city centre occupiers in notable buildings comprise organisations engaged in professional, scientific and technical activities; and financial and insurance activities. Information and communication, and real estate activities comprise an additional 15%. The public sector comprises only about 10%, being accommodated mainly in poorer quality office buildings. Other occupiers include companies engaged in construction, service activities, arts and recreation, supply of utilities, manufacturing, embassies and education. International companies engaged in the marketing and distribution of FMCG are not typically present in the city centre, preferring locations near the ring road such as Feniks or Megacenter. Tech companies are typically not found in the city centre either, preferring locations in green surroundings on the periphery of the city, such as the technology park or Imparo in Vič.

Changing market

The office market is by nature dynamic. During the financial crisis many companies moved to achieve savings, by downsizing and relocating to more energy efficient buildings. Things are different now, moves are generally prompted by expansion and the desire to work in better accommodation. Many startups are taking small units.

The project pipeline

Unfortunately the pipeline is unlikely to deliver much needed new office space soon. Šumi in the city centre is finally going ahead, but will have no office space. Tri Granit will not develop Emonika, they intended to sell the project to Prime Kapital, but the Romanian based developer has aborted from the acquisition due to planning difficulties. Tobačna is promising, but years away. An office project will be developed on the corner of Kajuhova and Letališka, but this is in the early stages and will take time to deliver.

The issue that has contributed most to the poor project pipeline is the lack of developers in Slovenia. Most large developers went out of business during the financial crisis. The few still operating got burned and have little appetite for speculative schemes. Some developers are growing, mainly those building small residential projects, but it will take a while before they are able to move on to large commercial developments. Banks are still reluctant to lend, having suffered huge losses.

Another issue is the high cost of building in Slovenia, and the low achievable rents. International companies only rent, they do not buy office space. There has been a big shift in the perception of local companies that now see the benefits of renting over buying. Typical rents in Class A buildings in Ljubljana are only 13€/m2/month, with a very few buildings able to achieve 16€/m2. Land is still expensive, and It is difficult for any developer to guarantee a profit, given these numbers.

Planning difficulties deter developers

It is difficult, costly, time consuming and bureaucratic to obtain building permission in Slovenia. New office projects are obliged to have a large ratio of parking/office, which makes building an office tower difficult. It is relatively easy to build three underground levels of parking, but expensive, difficult and risky to do more. This limits the potential height of the towers. Ljubljana desperately needs better public transport and fewer cars congesting the streets.

Wind downs

Some larger occupiers such as HETA and DUTB are in wind down procedures, and space in quality buildings will be freed up as a result. It is hard to say when though, given the unpredictable future of such organisations.

The outlook

The office market is going in only one direction. Before long there will be no availability of quality space. Landlords will be able to raise rents at lease renewal. There will be strong competition from tenants for any spaces that become available, driving prices up. Many tenants will have to take Class B and C space in order to relocate. The market has turned from tenant to landlord, and the time is finally right for new projects.

Jacqueline Stuart is a Director of S-Invest d.o.o.